The Right College.

The Right Price.

A Smarter Plan.

Expert college admissions and affordability guidance for families who want clarity, confidence, and smarter decisions.

Schedule a free parent strategy call and leave with a personalized plan for your family.

Recent student outcomes

Class of 2026 Results So Far

Admissions and scholarship results reported by students and families to date.

Recent admits included:

Vanderbilt, Georgia Tech, UNC Chapel Hill, Florida, Michigan, and more.

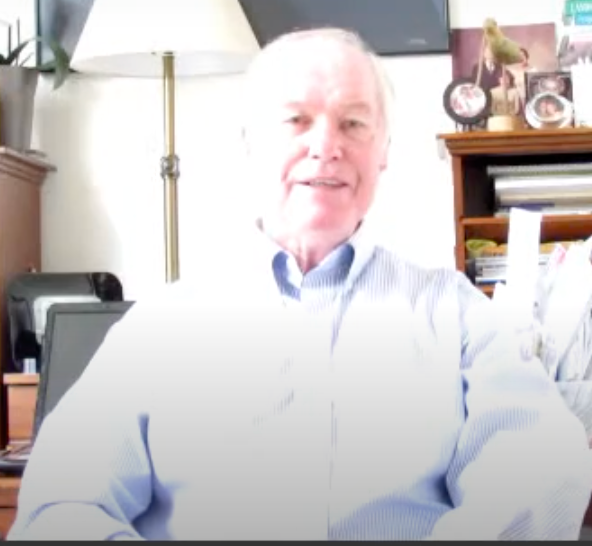

Hear from a recent student

College planning feels overhelming for a reason

Between rising costs, confusing applications, and pressure to make the right decision, many families feel stuck before they even begin.

Rising costs

Complicated applications

Scholarship and financial aid uncertainty

Pressure to make the right decision

We help families simplify the process, reduce stress, and move forward with a smarter plan.

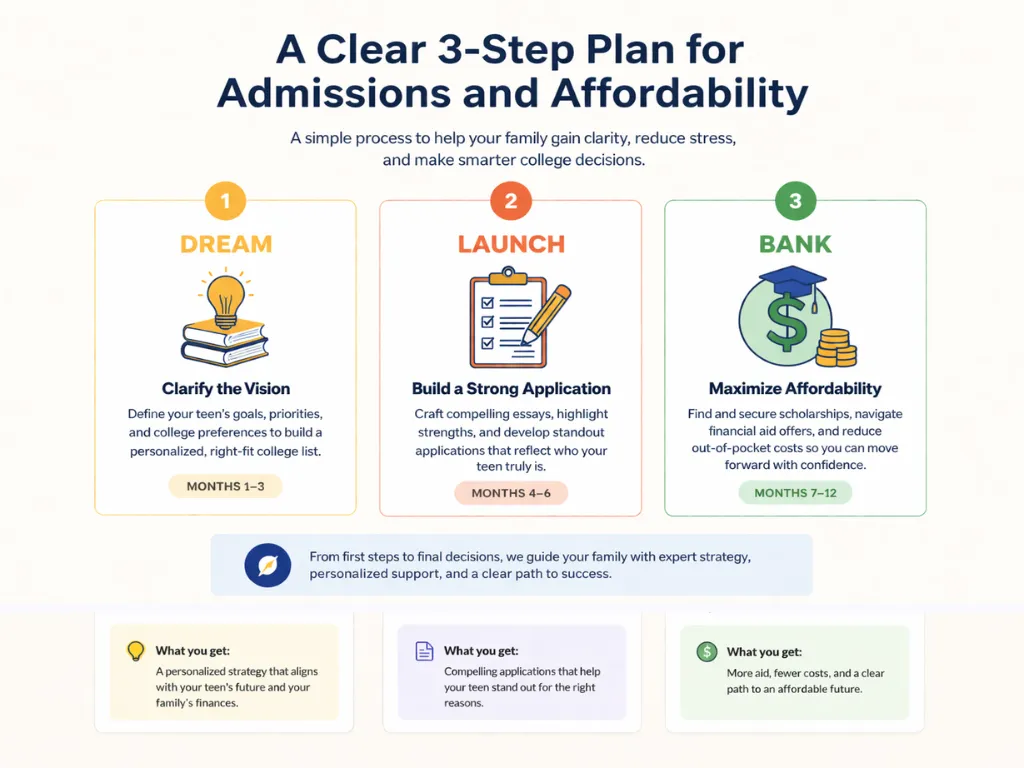

How the 3-Step Plan Helps Your Family

This may be the right fit for your family if....

We’re a strong fit for families who want clarity, support, and a smarter college plan.

Your teen wants a clearer admissions plan

You want help reducing tuition costs

You want support with applications, essays, and strategy

You feel overwhelmed by deadlines, choices, and financial aid

You want expert guidance without having to figure it all out alone

You want a smarter path to the right college at the right price

Just some of the colleges we’ve helped our students get into:

Victory Stories:

Real Families. Real Results. Real Savings.

We’ve helped over 1,200 families get into best-fit colleges—

while saving $40K–$60K each and removing the stress from college planning.

🎓 Hannah Witner

Over $1M in Scholarship Offers | Wake Forest + UNC

✅ Accepted to all 10 schools she applied to

✅ Family saved $75,000

✅ Used DREAM, LAUNCH, BANK system from day one

🗣️ “What seemed impossible became real. We couldn’t have done this alone.”

—Thomas Witner, Dad

🎓 Jack Noone

$168,000 in Scholarships | Mercer + USC

✅ Scholarships & acceptances in 6-months

✅ Saved $96,000 in out-of-pocket costs

✅ College selection & essay coaching made the difference

🗣️ “We needed structure for such a big financial decision. Thanks to Ryan, Jack earned $168,000 in scholarships and landed at his top-choice school.”

— John Noone, Dad

🎓Shane M.

Accepted to All 6 Colleges | $120,000 in Scholarships

✅ Customized college list and financial aid strategy

✅ Essay coaching and timeline accountability

✅ Graduating with zero student loan debt

🗣️ “Ryan and his team walked us through every step. Shane got into all six schools—and won’t owe a penny when he graduates.”

— Mack McCormick, Dad & Retired Teacher

🎓 Maya E.

$35,000 in Scholarships | Dream College Acceptance

✅ Strategic application and timeline planning

✅ Custom tools and personal guidance

✅ Saved time, reduced stress,

🗣️ “Saved the day & made all the difference in the world. They got us organized, gave us the tools—and helped us earn $35,000 in scholarships.”

— Helen Emish, Mom

Getting Started Is Simple

1. Schedule a Free Strategy Call

We'll learn your family's goals and answer your biggest questions.

2. Get Your Personalized Plan

You’ll walk away with a step-by-step strategy for admissions + financial aid.

3. Move Forward with Confidence

We’ll guide you through the entire process—essays, deadlines, aid, and all.

Spots are limited. Let’s get your teen on track today:

Clarity

Straightforward advice.

Integrity

Honesty and transparency.

Excellence

Top-notch services.

Contact Us

Ryan Clark, MBA, CCPS | College Admissions & Affordability Advisor

Address: 10130 Mallard Creek Rd, Suite 300, Charlotte, N.C. 28262

Tel: 704-944-3543

Email: [email protected]

FOLLOW US

LEGAL

Helping Families Become the Heroes of Their College Journey.

© Copyright 2025. Charlotte, NC. All Rights Reserved.